Most people complain about car insurance at some point. Monthly premiums can feel expensive, especially for younger drivers or families already dealing with rising living costs. Because of that, some people occasionally ask an interesting question: what would happen if car insurance simply stopped being mandatory in the United States?

At first glance, removing mandatory insurance laws might sound like a financial relief for millions of Americans. Drivers could choose whether they wanted coverage instead of being legally required to pay for it every month.

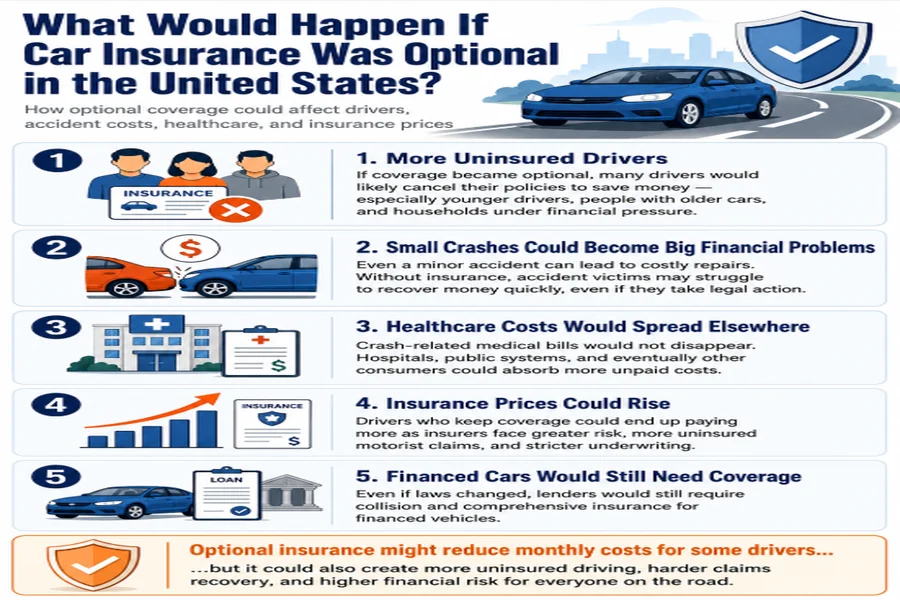

But once you look beyond the immediate savings, the situation becomes much more complicated.

A Minor Accident Could Become a Major Financial Problem

Imagine a hypothetical situation where a 19-year-old driver rear-ends another vehicle at a traffic light. The damage looks minor at first, but the repair estimate ends up costing $8,000 because modern vehicles contain expensive sensors, cameras, and electronic systems behind the bumpers.

If that young driver does not have insurance and only has a few hundred dollars in savings, the other driver may have no practical way to recover the money quickly. Even if a lawsuit is filed, collecting compensation could take years.

That is one of the main reasons mandatory insurance laws exist in the first place. They help guarantee that at least some financial protection exists after an accident.

Uninsured Drivers Would Likely Increase Quickly

Even with insurance requirements already in place, many states still struggle with uninsured motorists. If coverage became optional nationwide, millions of drivers would likely cancel their policies almost immediately.

This would especially affect:

- Younger drivers trying to reduce expenses

- Drivers with older vehicles

- People facing financial hardship

- Drivers who believe they are unlikely to crash

For many young adults, affordability is already one of the biggest challenges when shopping for coverage. Resources that explain low-upfront car insurance options can help newer drivers understand why maintaining at least basic protection is often worth the cost.

Healthcare Costs Could Spread Across the System

Car accidents do not only damage vehicles. Serious crashes can involve emergency room visits, surgeries, rehabilitation, physical therapy, and lost wages.

Without insurance, hospitals would likely absorb far more unpaid medical bills. Eventually, those losses could increase healthcare costs for everyone else through higher insurance premiums and public healthcare spending.

In other words, removing mandatory car insurance would not make accident costs disappear. It would simply move the financial burden somewhere else.

Insurance Companies Might Raise Prices

Ironically, drivers who continue carrying insurance could end up paying more.

Insurance companies calculate premiums based on risk. If uninsured driving becomes more common, insurers would face greater uncertainty and potentially larger payouts through uninsured motorist claims.

This could result in:

- Higher premiums

- More fraud investigations

- Stricter underwriting rules

- Increased legal disputes after accidents

Responsible drivers could ultimately pay higher prices to protect themselves from drivers who chose not to carry coverage.

Financed Cars Would Still Need Insurance

Even if state laws changed, many drivers would still be required to carry insurance because of their car loans.

Banks and lenders almost always require collision and comprehensive coverage while financing is active. That protects the lender’s financial interest in the vehicle.

This means optional insurance laws would mostly affect drivers who fully own their vehicles outright.

Would Roads Become More Dangerous?

Possibly — at least financially.

Removing mandatory insurance would not necessarily cause people to drive worse overnight. However, it could encourage riskier financial behavior because some drivers may feel they have less to lose after an accident.

In some situations, victims might avoid reporting smaller crashes entirely if they believe the at-fault driver has no ability to pay damages.

That could create a very different driving environment compared to today’s insurance-based system.

Some Drivers Would Support the Change

Not everyone would oppose removing insurance mandates. Supporters would likely argue that adults should be free to decide their own level of financial risk.

For people who rarely drive or own inexpensive vehicles, mandatory premiums can feel frustrating. Some would prefer saving the money and personally accepting the consequences if an accident occurs.

Others would argue that fewer regulations could create more competition and potentially lower insurance costs overall.

The Bigger Reality

The modern insurance system exists because vehicle accidents can create massive financial damage in seconds. Medical bills, lawsuits, lost wages, and repair costs can easily reach tens or hundreds of thousands of dollars.

Without mandatory insurance, many accident victims could struggle to recover compensation, while healthcare systems and courts would likely face greater pressure.

Although removing mandatory coverage might initially sound attractive from a cost-saving perspective, the long-term economic and legal consequences could be far more complicated than many people expect.